Homeownership comes with its fair share of responsibilities and challenges. A home isn’t just a space of comfort and refuge, but also a valuable asset that requires protection. Navigating the intricacies of home insurance can be complex, especially for new homeowners. With a variety of coverage options, policies, and terms, it’s essential to have a thorough understanding to secure a policy that ensures both peace of mind and financial security. This post aims to demystify home insurance, shedding light on its vital aspects, and providing actionable insights for every homeowner to make informed decisions. Knowing what to look for, asking the right questions, and understanding the coverage can transform a typically daunting task into a manageable and empowering experience.

The Basics Of Home Insurance

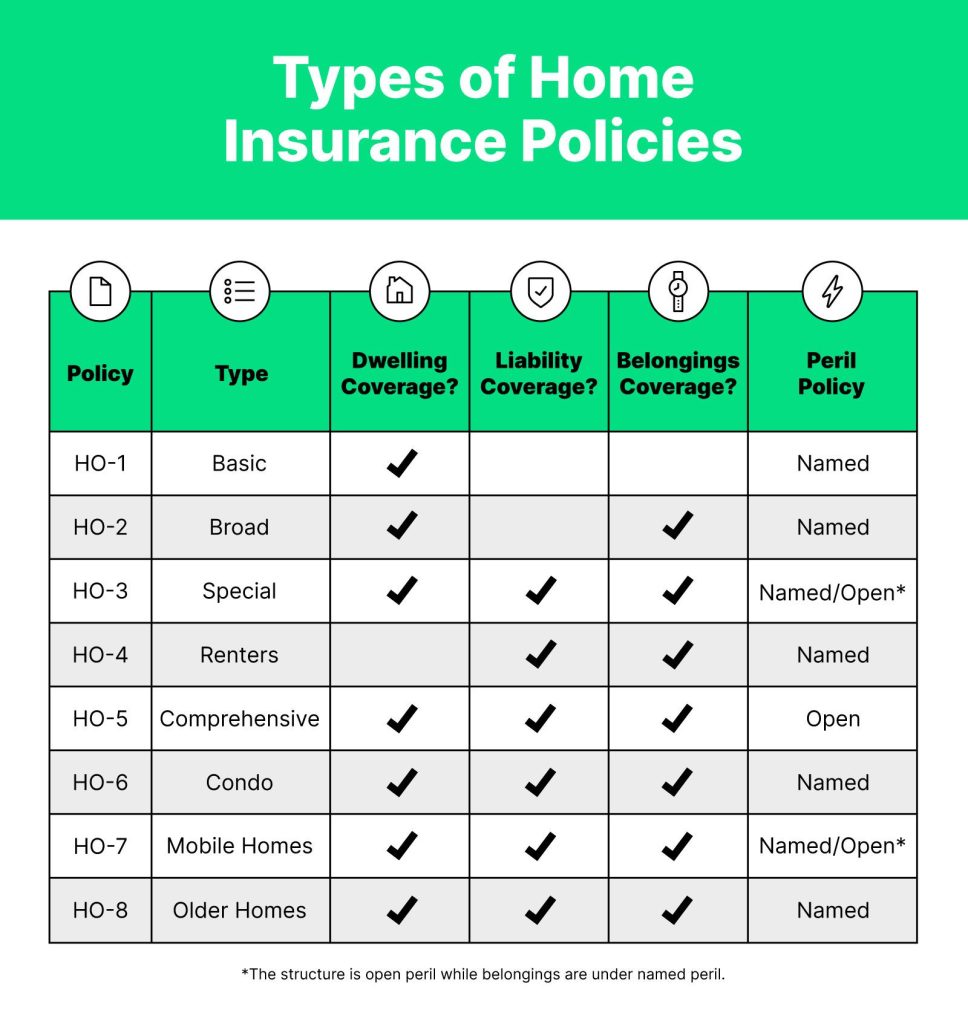

The myriad of home insurance options begins with understanding the different types of coverage available. Property damage coverage, for instance, protects against damage to the home and other structures on the property. Liability coverage offers protection in the event of injuries or property damage inflicted on others, while additional living expenses coverage assists homeowners if their home becomes uninhabitable due to a covered peril. Each type serves a distinct purpose, making it essential for homeowners to assess their specific needs and risks to select a well-rounded policy.

The consequences of underinsuring a home can be devastating. It’s a pitfall that many fall into, either in an attempt to save on premiums or due to a lack of awareness. Ensuring adequate coverage is crucial, as it determines the extent of financial protection in the event of unexpected occurrences like natural disasters, theft, or accidents. Homeowners should be vigilant in evaluating the cost of rebuilding or repairing their home, replacing personal belongings, and potential liability costs to avoid being caught off guard when disaster strikes.

How To Choose The Right Policy

Assessing individual insurance needs is the cornerstone of selecting the appropriate policy. Factors such as the type and location of the property, its contents, and the homeowner’s personal circumstances play a pivotal role in this process. Homeowners should also consider potential natural disasters and other risks specific to their location. A comprehensive assessment not only ensures adequate coverage but also aids in avoiding unnecessary costs for unneeded coverage.

Choosing an insurance provider requires careful consideration and comparison. Homeowners should explore the policies, premiums, and customer service reputation of multiple providers. Reading customer reviews, seeking recommendations, and considering the financial stability of the insurance companies can offer valuable insights. A provider that aligns with the homeowner’s needs, offers competitive premiums, and has a reputation for excellent service and claim handling can be a reliable choice for a long-term partnership.

Factors That Affect Premiums

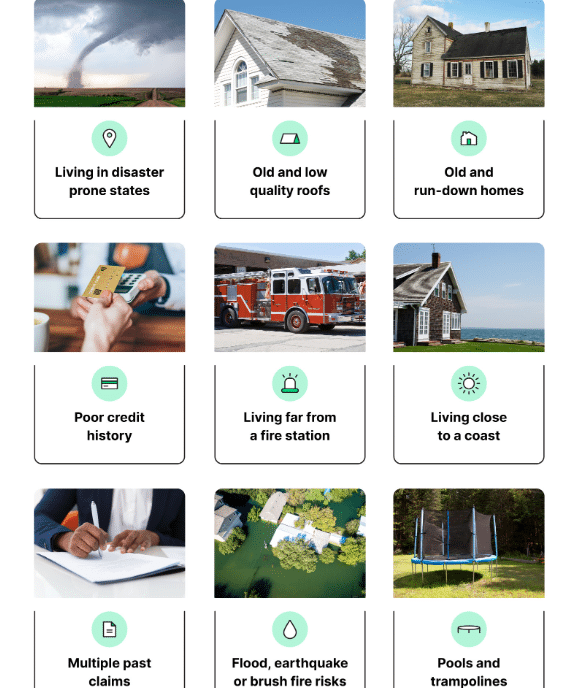

The home’s value and condition are instrumental in determining insurance premiums. Older homes or those in poor condition often attract higher premiums due to the increased risk of damage and the potential for costly repairs. Home renovations and improvements can lead to a reevaluation and reduction in premiums, as a well-maintained home is generally considered to be at a lower risk for insurance claims. The material used in construction, the home’s overall design, and safety features can also influence the cost of insurance.

Location plays a significant role in insurance costs, with areas prone to natural disasters or with high crime rates typically experiencing higher premiums. Homeowners in these regions often need to consider additional coverages or higher policy limits to mitigate their unique risks. Proximity to emergency services like fire departments can also impact insurance costs. Factors such as neighborhood safety, the local climate, and the area’s claim history are all meticulously evaluated to calculate premiums.